A Boost in the Number of European Small Claims Procedures before Spanish Courts: A Collateral Effect of the Massive Number of Applications for European Payment Orders?

Carlos Santaló Goris, Researcher at the Max Planck Institute Luxembourg for International, European and Regulatory Procedural Law and Ph.D. candidate at the University of Luxembourg, offers an analysis of the Spanish statistics on the European Small Claims Procedure.

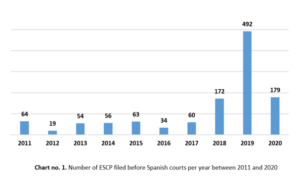

Until 2017, the annual number of European Small Claims Proceedings (“ESCP”) in Spain was relatively small, with an average of 50 ESCPs per year. With some exceptions, this minimal use of the ESCP fits the general trend across Europe (Deloitte Report). However, from 2017 to 2018 the number of ESCPs in Spain increased 286,6%. Against the 60 ESCPs issued in 2017, 172 were issued in 2020. In 2019, the number of ESCPs continued climbing to 492 ESCPs. This trend reversed in 2020, when there were just 179 ESCPs.

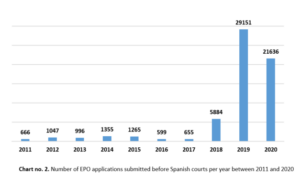

The use of the Regulation establishing the European Payment Order (“EPO Regulation”) experienced a similar fluctuation between 2018 and 2020. Since its entry into force, the EPO Regulation was significantly more prevalent among Spanish creditors than the ESCP Regulation. Between 2011 to 2020, there were an average of 940 EPO applications per year. Nonetheless, from 2017 to 2019, the number of EPO applications increased 4.451%: just in 2019, 29,151 EPOs were issued in Spain. In 2020, the number of EPOs decreased to 21,636. the massive boost in EPO applications results from creditors’ attempts to circumvent EU consumer protection standards under the Spanish domestic payment order.

From Banco Español de Crédito to Bondora

After the CJEU judgment C-618/10, Banco Español de Crédito, the Spanish legislator amended the Spanish Code of Civil Procedure to impose on courts a mandatory review of the fairness of the contractual terms in a request for a domestic payment order. Creditors noticed that they could circumvent such control through the EPO. Unlike the Spanish payment order, the EPO is a non-documentary type payment order. For an EPO, standard form creditors only have to indicate “the cause of the action, including a description of the circumstances invoked as the basis of the claim” as well as “a description of evidence supporting the claim” (Article 7(2) EPO Regulation). Moreover, the Spanish legislation implementing the EPO states that courts have to reject any other documentation beyond the EPO application standard form. Creditors realized that in this manner there was no possible way for the court to examine the fairness of the contratual terms in EPOs against consumers. Consequently, the number of EPO applications between 2017 and 2019 increased remarkably.

In some cases, a claim’s cross-border dimension was even fabricated to access the EPO Regulation. The EPO, like the ESCP, is only applicable in cross-border claims, which means that “at least one of the parties is domiciled or habitually resident in a Member State other than the Member State of the court seised”(Article 3 EPO Regulation). Against this background, creditors assigned the debt to a creditor abroad (in many cases, vulture funds and companies specialized in debt recovery) in order to transform a purely internal claim into a cross-border one.

The abnormal increase in the number of EPOs did not go unnoticed among Spanish judges. Three Spanish courts decided to submit preliminary references to the CJEU, asking, precisely, whether it is possible to examine the fairness of the contractual terms in an EPO application requested against a consumer. Two of these preliminary references led to the judgment Joined Cases C?453/18 and C?494/18, Bondora, where the CJEU replied positively, acknowledging that courts can examine the fairness of the contractual terms (on this judgment, see this previous post). The judgment was rendered in December 2019. In 2020, the number of EPOs started to decrease. It appears that after Bondora the EPO became less attractive to creditors.

The connection between the EPO and the ESCP Regulation

At this point one needs to ask how the increase in the use of the EPO Regulation has had an impact on the use of the ESCP Regulation. The answer is likely found in the 2015 joint reform of the EPO and ESCP Regulations (Regulation (EU) 2015/2421). Among other changes, this reform introduced an amendment in the EPO Regulation which allows, once the creditor lodges a statement of opposition against an EPO, for an automatic continuation of proceedings under the ESCP (Article 17(1)(a) EPO Regulation). For this to happen, creditors simply need to state their intention by making use of a code in the EPO application standard form. It appears that, in Spain, many of those creditors who applied for an EPO in order to circumvent consumer protection standards under the domestic payment order found in the ESCP a subsdiary proceeding if debtors opposed the EPO.

An isolated Spanish phenomenon?

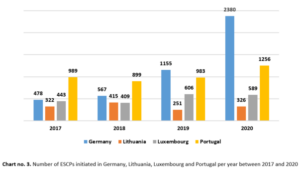

Statistics in Spain show that, at least in this Member State, the connection between the EPO and ESCP Regulations functions and gives more visibility to the ESCP. The lack of awareness about the ESCP Regulation was one of the issues that the Commission aimed to tackle with the 2015 reform. One might wonder if a similar increase in the use of the ESCP could be appreciated in other Member States. Available public statistics in Portugal, Lithuania, and Luxembourg do not reveal any significant change in the use of the ESCP after 2017, the year the amendment entered into force. In Lithuania, the number of ESCPs even decreased from 2018 to 2019.

Conversely, in Germany, statistics reveal a steady growth over those years. Against the 478 ESCPs issued in Germany in 2017, 2380 ESCP were issued in 2020, standing for an increase of 498%. Perhaps, after an unsuccessful start, the ESCP Regulation is finally bearing fruit.